Quarterly Newsletter to Public Q4 2013

January 13, 2014

“Concentrating the majority of one’s investment portfolio in one investment category (such as the US stock market) based on an unknowable and fickle long-term equity premium, is a dangerous game of 'probability chicken.'”

Peter Bernstein, Economic Historian and Author of Against the Gods, the Remarkable Story of Risk.

Executive Summary

Despite most investors’ perception, 2013 was not a good year for most asset classes. Global View Portfolios, like most smart money investors, were conservatively positioned in a continued global recessionary growth environment and lagged major indexes. We are happy to have achieved positive returns in this economic environment.

- Despite a good year for Developed Country Stock markets, the majority of asset classes, and smart money investors, did not do well in 2013. At this juncture, prudent investors should be looking outside of the large company developed world universe to find positive returns going forward.

- Broad market stock index performance in 2013 is largely attributable to excess liquidity created by the world’s central banks.

- Our bellwether for economic performance, ECRI, continues to believe the global economy is in a mild recessionary state. Fewer jobs were created in 2013 than 2012. One formerly bearish economist, Dave Rosenberg, has become more constructive so we are watching the data closely.

- We conducted a due diligence trip to the West Coast in November to assess our managers and gain confidence in their investment strategies. We learned of opportunity outside of the US that we hope to capture going forward.

- Over the last 20 years, individual investors with “do it yourself” strategies have been unable to keep up with inflation. Chasing recent performance is the fastest way to erode capital. Unfortunately “do it yourselfers” do not have access to foreign investment markets on their own and are unlikely to own the world’s cheapest assets.

- Our portfolios have become increasingly conservative as valuations have climbed, with low sensitivity to rising interest rates and falling stock market prices; however, we are constructively taking risk in out of favor and undervalued areas particularly outside of the United States and in Emerging Markets for clients who can withstand volatility and have a long time horizon.

Broad Market Index Performance not Illustrative of Asset Class and Smart Money Returns

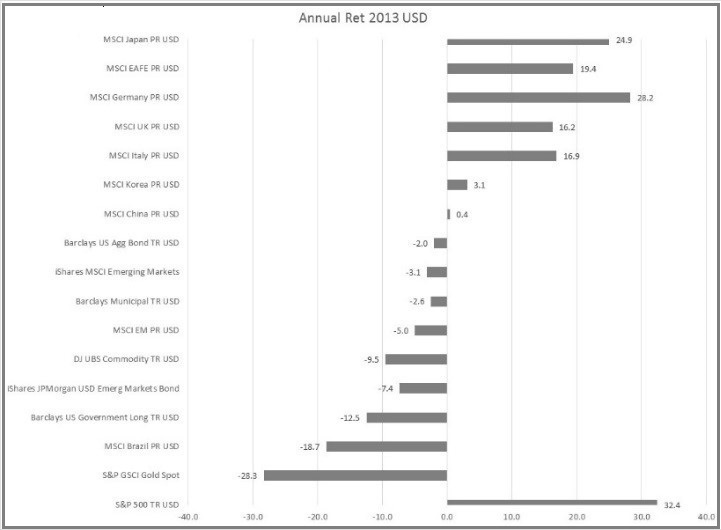

Unsophisticated investors watching CNBC are led to  believe 2013 was the best year for assets in decades. They are right if one invested in the US stock market and did not diversify internationally into emerging markets or own commodities such as gold. 2013 was a year that rewarded imprudence and punished prudence.

believe 2013 was the best year for assets in decades. They are right if one invested in the US stock market and did not diversify internationally into emerging markets or own commodities such as gold. 2013 was a year that rewarded imprudence and punished prudence.

Some of the best managers in the world with strong track records of high performance and low volatility suffered very low returns. As the chart illustrates, Bonds fell 2% overall in 2013, Emerging Market stocks were down 3.1%, Emerging Market bonds were down 7.4%, and gold was down 28%. As a consequence some more risk-averse managers suffered losses in 2013. For example, the Bridgewater All-Weather 12% Volatility portfolio suffered a loss 4.6% despite having returned 12.6% per year for the last 5 years with a very low standard deviation of 8.5. This poor performance was largely attributable to a bet on rising inflation in an improving economy. Unfortunately inflation fell signaling a weaker economy.

Similarly Bridgewater’s version of a Long-Term portfolio, his Pure Alpha 18% Volatility Portfolio, made 5.6% despite having returned 13.6% per year since its inception in 1991.

Our colleagues at Research Affiliates use cyclically adjusted valuations, specifically the Cyclically Adjusted Price to Earnings Ratio or CAPE, as a predictor for future returns. At the end of 2012, the CAPE for the US was 21 versus its long-term average of 16.5, suggesting stocks were overvalued by about 30%. At that time the CAPE for Emerging markets was 15, versus its long-term average of 16, suggesting these markets were undervalued. However, as the chart above illustrates US stocks rose 32% while Emerging Market stocks fell 3.1%.

The CNBC investor, chasing last year’s return, may find US stocks attractive. The prudent investor might look at valuations. The current US CAPE of about 25.5 implies stocks are over 50% overvalued assuming valuations revert to their mean of 16.5. Interestingly, using similar metrics Emerging Markets trade at a slight discount. However, Research Affiliates, which conducts a fundamental weighting for a far larger opportunity set, recently stated that their index trades at a CAPE of 9. Should this mean revert there is potential for over 67% gain. Remember, a 40% loss requires a 67% gain to recover. US index investors as well as international and emerging market index investors should take note. Prudent investors should be broadly diversified, avoiding overvalued broad asset classes. This is an environment where stock pickers in these markets are set up for strong outperformance.

Easy Money, Rising Stock Markets

We have talked about, ad nauseum, the unprecedented monetary policy of the world’s central banks. While the US has “tapered” its Quantitative Easing program by $10 billion a month, the Fed continues to print $75 billion a month. The Japanese response is over 3 times as large in relation to its economy. Moreover, the European Central Bank maintains an easy money policy and is likely to continue printing.

The chart here clearly illustrates that prices in the US and Europe have risen almost entirely due to investor’s willingness to pay more (expansion in Price/Earnings multiple) as opposed to fundamentals (earnings per share change). While the US did experience growth in earnings per share this is largely due to company share buy backs, i.e. earnings per share grew primarily because there were fewer shares not because of phenomenal earnings growth. European companies experienced hardly any growth. On the other hand, Japanese stock prices rose primarily due to an increase in earnings as the economy rebounded.

While we cannot know what the future holds, we suspect this era of easy money will last a very long time as the world’s developed economies attempt to “beautifully” reduce their indebtedness (delever) by printing money to create inflation and nominal economic growth greater than their cost of indebtedness.

Economic Growth Remains Recessionary

There were fewer jobs created in the US in 2013 than in 2012. According to the Establishment Survey, 2.193 million jobs were created in 2012 versus 2.186 in 2013. While there is much talk of a pickup in economic growth in the US, this had not yet materialized despite reduced unemployment due to a falling labor participation rate. Global growth remains weak. Japan has entered an economic slowdown and parts of Europe are weakening.

We fear the current economic growth environment will remain weak for some time and that the world’s central banks will continue to create money to fill the gap in credit creation. We know that the person who created this thesis, Ray Dalio, at Bridgewater, appears to believe its ability to navigate this appropriately is tenuous, and has taken a low risk stance. ECRI recently re-iterated their recession call. Specifically, they believe the epicenter of the recession occurred from Q4 2012-Q1 2013 when real GDP was 0.6%. They believe it is quite likely that this will be revised downward. It is not uncommon for NBER to revise data down from 2-4% when a recession is recognized. The next major data revision will happen in July of this year.

Dave Rosenberg is our Devil’s Advocate to  ECRI on the economy. Dave believes 2014 will be the year of the horse which will break out. His rationale is that fiscal headwinds are subsiding, that US companies are flush with cash and must invest in new equipment, and that the US consumer is delevered. Because we respect Dave we like to read his opinion and will continue to watch him. It is likely that ECRI will signal this when it happens. Despite his opinion on the economy, Dave is hardly bullish on the US stock market.

ECRI on the economy. Dave believes 2014 will be the year of the horse which will break out. His rationale is that fiscal headwinds are subsiding, that US companies are flush with cash and must invest in new equipment, and that the US consumer is delevered. Because we respect Dave we like to read his opinion and will continue to watch him. It is likely that ECRI will signal this when it happens. Despite his opinion on the economy, Dave is hardly bullish on the US stock market.

.\

Visit with Fund Managers on the West Coast

We recently visited three of our favorite fund managers on the West Coast to gain insight into their current investment outlook. The highlight of the visit was with Grandeur Peaks in Salt Lake City.

See Manager Due Diligence Trip below.

The “Do It Yourself” Fallacy

Investors buying stocks in 2013 are probably pretty happy with themselves. Investors typically don’t have access to overseas exchanges, so unless they bought Exchange Traded Funds or mutual funds holding overseas stocks, they probably owned the US market. As Daniel Kahnemann proved, human beings are likely to extrapolate the recent past into the indefinite future and overly attribute their success to their own ability. While we cannot know the future, we can show that individual investors were unable to keep up with inflation over the last 20 years. We fear they will continue the pattern, chase performance, and be punished once again.

Investors buying stocks in 2013 are probably pretty happy with themselves. Investors typically don’t have access to overseas exchanges, so unless they bought Exchange Traded Funds or mutual funds holding overseas stocks, they probably owned the US market. As Daniel Kahnemann proved, human beings are likely to extrapolate the recent past into the indefinite future and overly attribute their success to their own ability. While we cannot know the future, we can show that individual investors were unable to keep up with inflation over the last 20 years. We fear they will continue the pattern, chase performance, and be punished once again.

Next Steps

Our decision to reduce risk over two years ago was warranted by overwhelming historical evidence and has been validated by actions of some of the world’s smartest investors. Valuations in the US and broad developed markets are close to their levels in 2000 and 2007, therefore this is not a time to make a wholesale increase in risk without more clarity on economic growth.

However, because not all asset classes participated in the Central Bank Liquidity fueled rally that affected the US market last year, there are increasing signs of opportunities available in Emerging markets as well as in smaller companies and cyclical companies in Europe and Asia. Since our Long-Term Less Volatile managers raised cash levels and reduced overall exposure to risk assets as they found it more difficult to find opportunities outside of the broader world indexes, our portfolios have become more conservative than we envisioned they might be.

Our managers seek out opportunities company by company. Disparities exist that we are capable of gaining access to through relationships we have established that are quite simply not available to most investors. For this reason we ardently strive to opportunely add appropriate risk to our Long-Term portfolios especially when we feel the opportunity to do so may be short-lived, i.e. the funds may permanently close to new investors.

We will be conducting client reviews to ascertain the appropriate level of risk for all of our clients and discuss the current investment landscape. As always, we are very grateful that you have chosen us and your investment advisor and look forward to working with you for many years.