Everybody knows that investing has risks. But imagine if you could invest “risk free.” Sounds good, right?

The problem is that when you shine a light on these promises they turn out to be hollow.

In fact, the living benefits insurance companies promise might just be monopoly money.

Let’s have a look. Insurance companies, through insurance firms, big banks, and often (unfortunately) even through “fee-based” firms, sell their clients variable annuities that promise they can take a set percentage (5% or 6%) as income for the rest of their life.

Many investors find this appealing because they don’t want to lose money. The problem is that it comes at a high cost. When you buy a variable annuity you have to pay in multiple ways (that you never see):

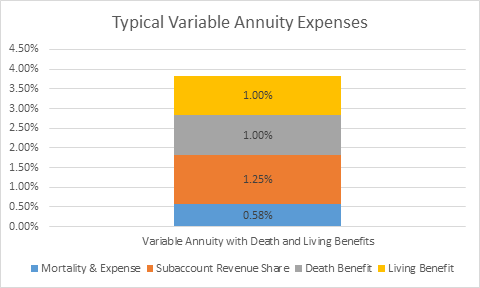

As the chart illustrates there are four key ongoing annual expenses in variable annuities (most are avoidable for savvy investors). The Mortality and Expense, Subaccount Revenue Share, Death Benefit and Living Benefit can easily add up to 4% p.a. (before we even include the cost of the investments).

there are four key ongoing annual expenses in variable annuities (most are avoidable for savvy investors). The Mortality and Expense, Subaccount Revenue Share, Death Benefit and Living Benefit can easily add up to 4% p.a. (before we even include the cost of the investments).

In other words, the investments in the annuity have to make about 4% more per year than similar investments outside of the annuity JUST TO BREAK EVEN.

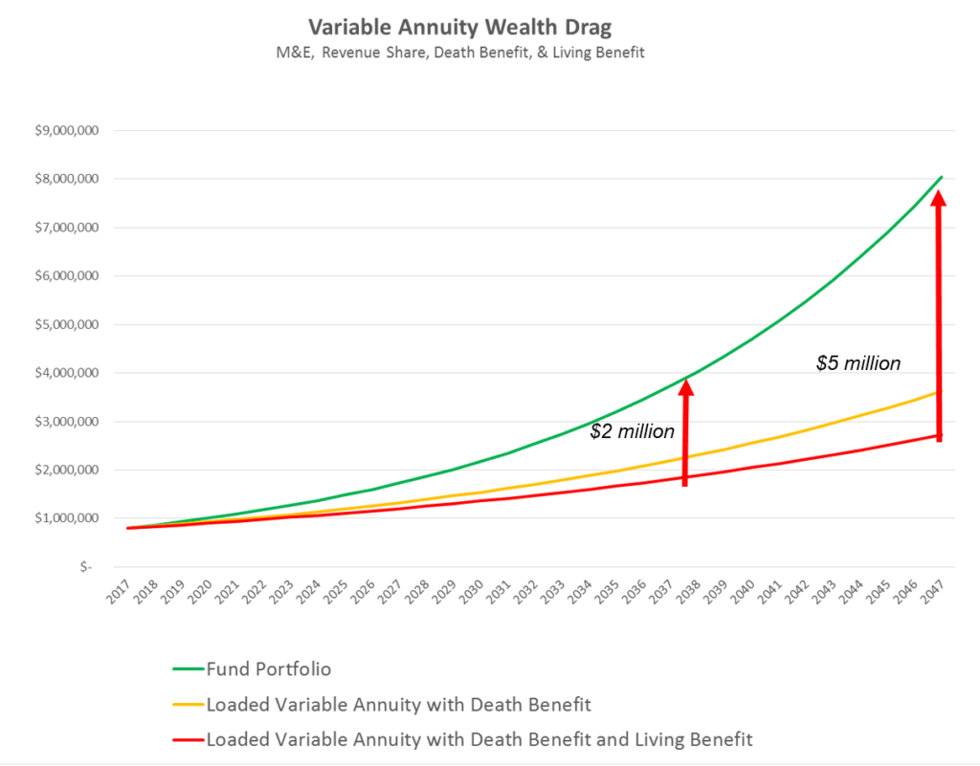

Let’s look at how that impacts your wealth. We had a client with $800,000 to invest that was shown an illustration by an unscrupulous insurance agent to invest in a product that had fees like this. Assuming an investment made 8% per year after fees (in green), an investor in the fund would have about $2 million more than the Annuity after 20 years and $5 million after 30 years. While the effect is less if you forego the living benefit, it is significant.

You are not stupid.

Because you now know (it’s REAL money, not monopoly money) you will think twice before making this investment.

But if you are still intrigued by a “5-6%” Guaranteed Minimum Lifetime Income guarantee, be aware of this:

- Most of the time these benefits go unexercised, which means they are simply a transfer of wealth from the beneficiary to the insurance company because most annuities end up paying a death benefit of the amount of premiums or contract value. They do not pay beneficiaries the “guaranteed” income benefit value.

- If the benefit is exercised it is rarely hedged against inflation, which means high inflation will erode the benefit. Add this to the fees and you transfer wealth to the insurance company.

- If the benefit is exercised and you need more than 7% or so in a given year (every policy is different) YOU LOSE THE GUARANTEE, which means the annuity falls back to its contract value.

So think about it. If a 5% guaranteed minimum income guarantee is exercised when you are 70 years old, and you live to 90, all you get back is a return of principal. In other words you get your own money back.

At Global View, our team of Certified Planning Professional™ financial planners, accountant, and tax attorney work hard to educate our clients and make investments that are not only suitable for them, but that are also in their best interests first. We are not just fee-based, we are fee-only. We never get paid by anyone other than our clients.

We have yet to find a loaded annuity that we believe is in our clients’ best interest first, but if we do we’ll tell you.

Instead we have strategies to RESCUE investors from inappropriate, high cost annuities. These include our low-cost, tax efficient stock portfolios as well as access to boutique managers that simply won’t pay to play with the larger banks and insurance companies. Whether your goal is to make 5% per year, 8% per year, or more, we have strategies designed to do this.

We, and our managers all invest alongside our clients. Which means instead of investing other people’s money, we have skin in the game.